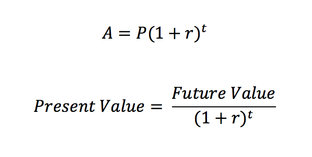

There are a litany of applause-winning complaints about education that are either outdated or foolish. History teachers often hear, “What is the point of memorizing all these dates?” The reality is that few history curricula used in the United States in the past thirty years have included memorizing dates. No standardized history exam, from the SAT to the AP to the NY State Regents, has tested dates at all in more than a generation. Math teachers are often annoyed with, “Why are we learning trigonometry? Why can’t you teach me something useful, like balancing a checkbook?” First of all, many textbooks do teach simple money management. It’s boring and easy, which is why you forgot it. Second, you don’t really need to know how to balance a checkbook anymore, so shut up. A suggestion: the time value of money, or the (net) present value, would be an excellent addition to any algebra class. Most math teachers teach a closely related subject: compound interest. But present value is surprisingly rare. To be clear, present value is the idea that money earned in the future is worth less than the same amount earned today. The formula for present value is almost identical to the formula for compound interest (making it an excellent review topic, a great way to discuss manipulating algebra, and an easy way to show how to derive formulas):  The concept appeals to the “teach me something useful” crowd and lends itself to fun, engaging word problems that mimic real world business decisions. The difficulty can be scaled all the way up to the university level and down to bright middle-schoolers. It also has a moral dimension, quantifying Ben Franklin’s adage, “time is money.”

Here are two problems for your enjoyment: 1. A friend of ours is going away for a little while. He promises to pay you back $300,000 in 2020 if you lend him $200,000 today. You have access to a CD that offers 10% interest. What is the net present value of the investment? Is it worth it? 2. Another friend of yours wants to start a food truck selling curried tacos (Mexicali Masala!) in NYC. He asks you for $50,000, and promises to pay back a bit every year according to the following schedule: $2000 after one year, $4000 after two years, $8000 after three years, $16,000 after four years, and $32,000 after five years. If you have access to a bank account that pays 5% interest, should you make this investment? What is the net present value of the investment? P.S.: The man pictured at the top is Bobby "Bacala," the loan shark from the Sopranos, who has excellent methods for teaching the time value of money.

0 Comments

|

AuthorI'm an entrepreneur and I teach math, history, economics, and fitness. I'm looking for arguments. Archives

November 2019

|

RSS Feed

RSS Feed